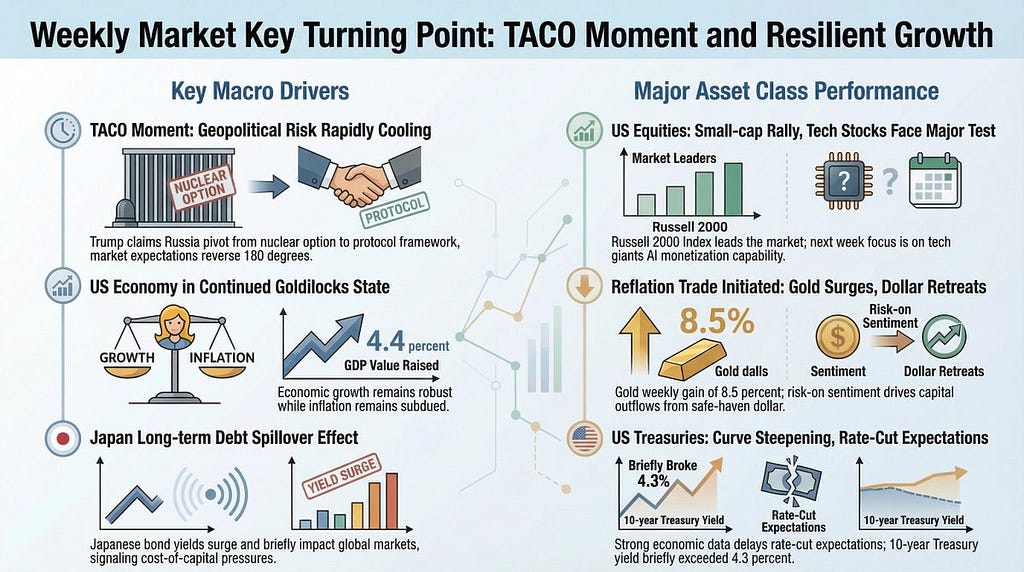

From “Maximum Pressure” to the “TACO Moment”

Trump’s tariffs are a “feint,” but the resilience of the U.S. economy is “real muscle.” Next week, all eyes are on the earnings season — specifically whether tech giants like Microsoft and Apple can justify massive AI CAPEX through monetization efficiency.

Macro Events

- The Greenland Plot Twist: At the start of the week, Trump’s “tariff nuke” over the Greenland acquisition triggered a “triple kill” in U.S. stocks, bonds, and forex. However, he pivoted sharply (TACO) at Davos midweek, announcing a “framework agreement” and suspending the February 1st tariff hike. Market sentiment instantly flipped from “war footing” back to “growth expectations.”

- JGB “Spillover”: Sanae Takaichi’s announcement to dissolve the Diet sparked expectations of fiscal expansion. The 40-year JGB yield briefly surged past 4%, dragging long-end U.S. Treasury yields higher before retreating as global funding pressures eased slightly.

- The “Goldilocks” Economy: Final GDP was revised up to 4.4%, and PPI met expectations. This combination of resilient growth and stable inflation has led the market to price in a “Higher for Longer” interest rate environment, effectively killing hopes for a Q1 rate cut.

Market Performance

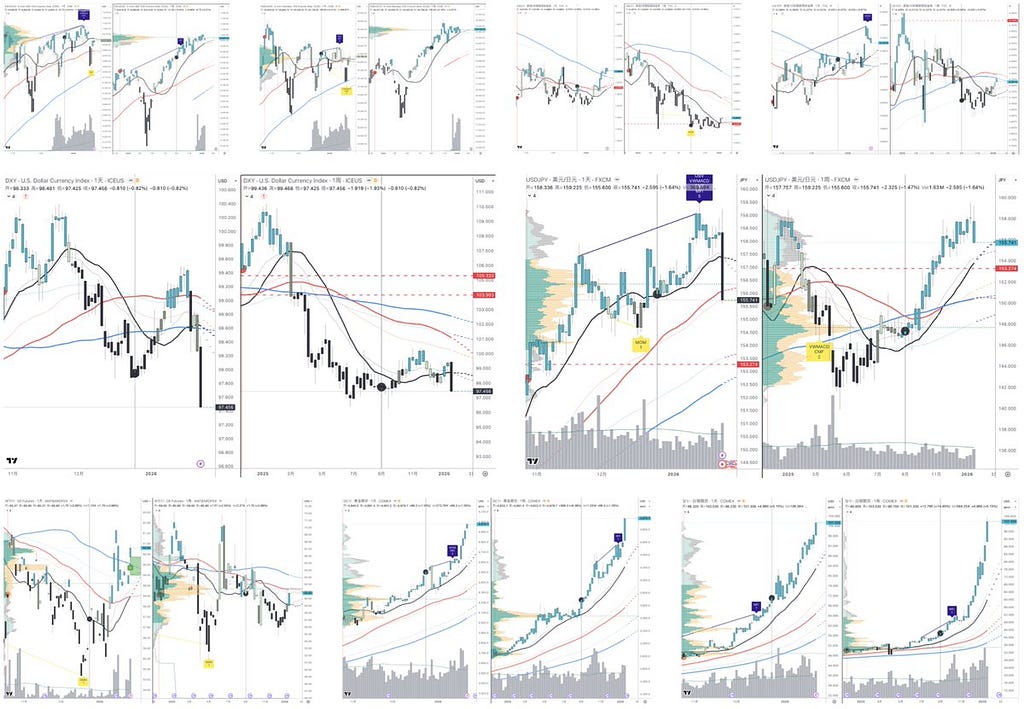

- U.S. Equities: The Small-Cap Catch-up Rally. The S&P 500 slipped 0.42% this week despite a counterattack from tech giants (led by Meta). However, the Russell 2000 (small caps) stole the show with a 15-day winning streak. Retail investors are aggressively “buying the dip” in laggard sectors.

- Treasuries: Divergence Between Ends. Impacted by JGB volatility and strong GDP data, the 10-year yield briefly breached 4.3%. Barring actual geopolitical conflict, the 4.2%–4.3% range offers value for long-term allocation. The short end remains volatile and elevated as rate-cut expectations are pushed back.

- USD: Counter-intuitive Retreat. Despite economic strength, the DXY fell below the 98 level. This reflects a return of risk appetite, with capital flowing from the “safe-haven” greenback into equities and precious metals. The dollar’s hegemony faces “slow erosion.”

- Precious Metals: Prelude to Gold 5000. Gold surged 8.5% in a single week, while Silver made a historic breakthrough above $100! The narrative has evolved from “safe-haven” to a “reflation trade.” Even as geopolitics cool, structural concerns over long-term USD credit will continue to drive gold higher.

- Crude Oil: Geopolitical De-escalation. Following the eased tariff threats, oil recovered after dipping below $60. Assuming no substantive conflict in the Middle East or Greenland, oil is likely to oscillate within the $60–$70 range.

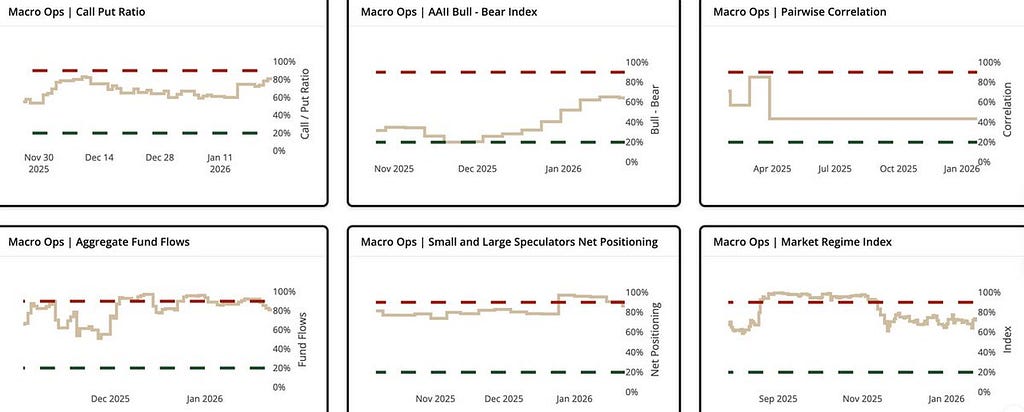

[US Equities: A “Covered Retreat” by Tech Giants]

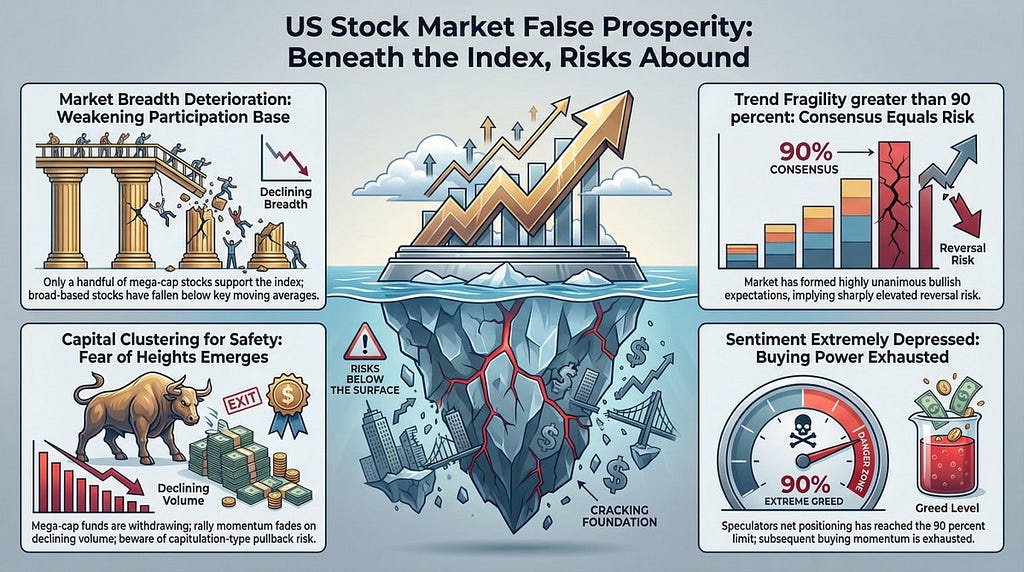

While the S&P 500 appears resilient, the underlying foundation is fracturing.

1.Erosion of Market Breadth: Breadth indicators show that while indices are at highs, fewer stocks remain above their moving averages. This is “phantom prosperity” — a few tech giants are holding the line while the majority of companies retreat.

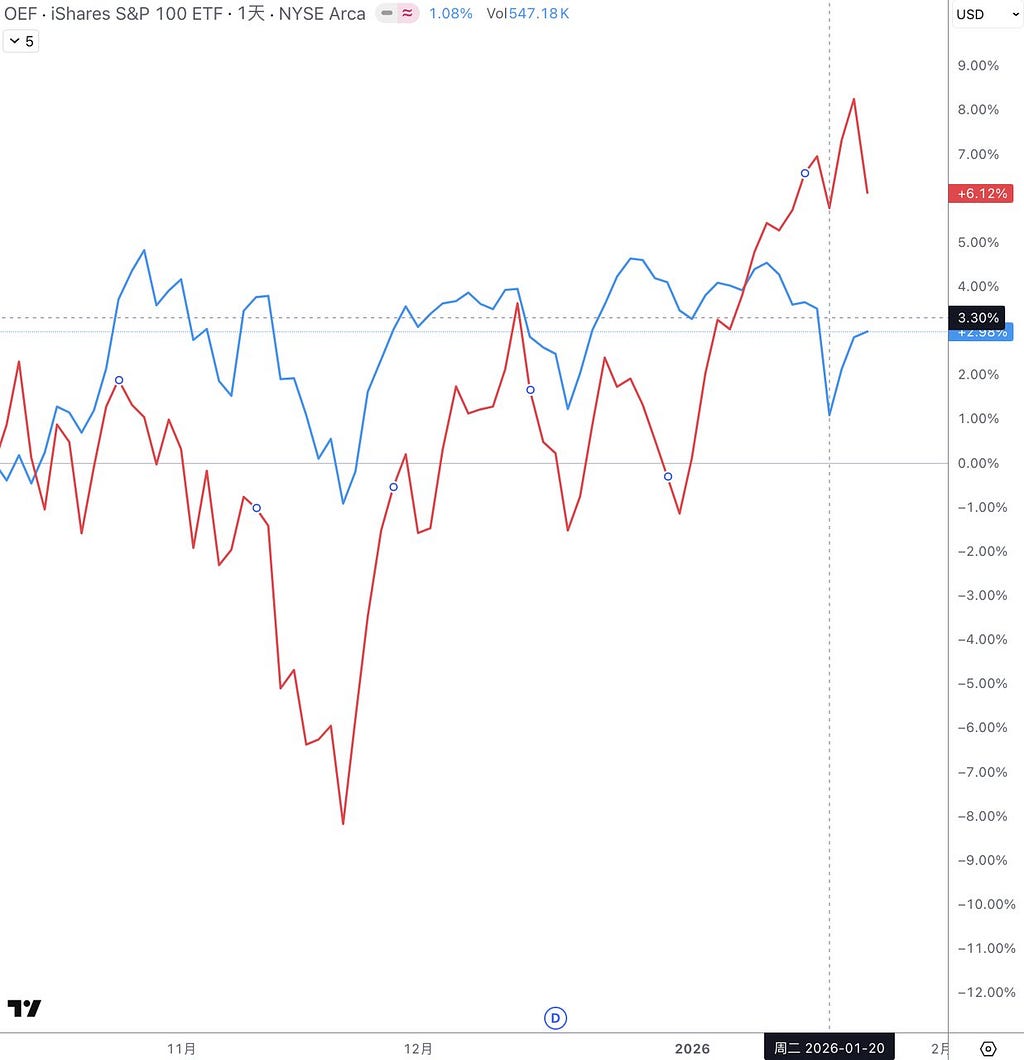

2.Safe-Haven Concentration: The divergence between Mega-caps (OEF) and Small-cap Growth (IWO) has reached extremes. Institutional capital is huddling in “Behemoths” like NVIDIA and Apple, fearing small-cap exposure. This “vertigo-induced” crowding is often a terminal signal for a rally.

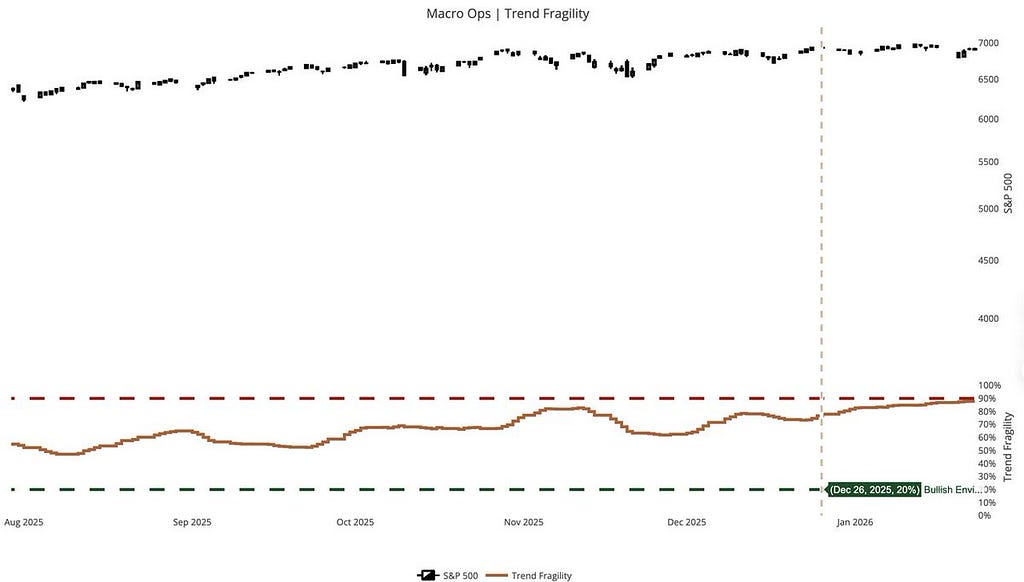

3.Paper-Thin Trends: “Trend Fragility” has hit the 90% red line. The market is saturated with “consensus expectations.” In macro logic, when everyone is bullish, the danger is at its peak.

4.Sentiment: Rampant Greed. AAII retail confidence has hit 64%, with Call option ratios remaining at a staggering 81%. The most alarming signal: Speculator net positions are at the 90% limit, suggesting that those who want to gamble are fully leveraged, and subsequent buying power has dried up.

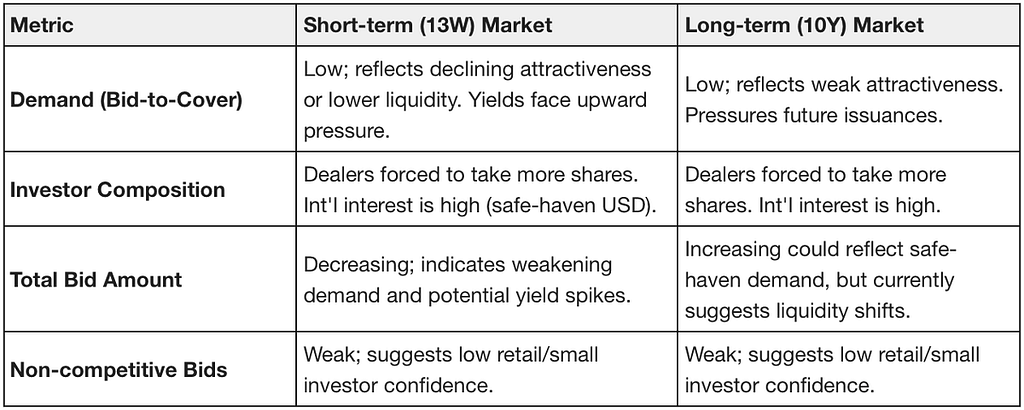

[U.S. Treasuries]

- Rates: The 96% “Apathetic” Consensus. The probability of holding rates steady on Jan 28 sits at a locked 96%. Last year’s rate-cut dreams have shattered. The reality: as long as the Fed stays hawkish, short-end rates are an immovable object. Avoid over-extending duration; the elasticity for upward rate movement remains.

- Yield Spreads Shrinking: Is the market doubting growth momentum? Spreads for 30Y-2Y and 10Y-3M are narrowing. Long-end yields are falling faster than the short-end, suggesting capital is “hiding” in long bonds. While still positive, the market is correcting previously overheated growth expectations.

- Primary Market: Retail Exit, Dealers Filling the Gap. Short-term (13-Week): Institutions are holding firm, but retail exit signals are strong (allotted shares halved). Patience for cash is thinning as short-end yields lose their luster. Long-term (10-Year): Demand is flagging. Bid-to-cover ratios have dropped below the average, forcing primary dealers to absorb the supply. This is a precursor to upward pressure on yields — if. If international whales don’t step in, long-end rates will be hard to suppress.

[Commodities]

Gold ETF Holdings & Central Bank Activity:

- Global Gold ETF holdings rose last week alongside prices.

- PBOC: The Chinese central bank increased gold reserves for the 14th consecutive month. December reserves hit 74.15 million ounces (+30k oz MoM). Total FX reserves rose to $3.3579 trillion (+0.34% MoM).

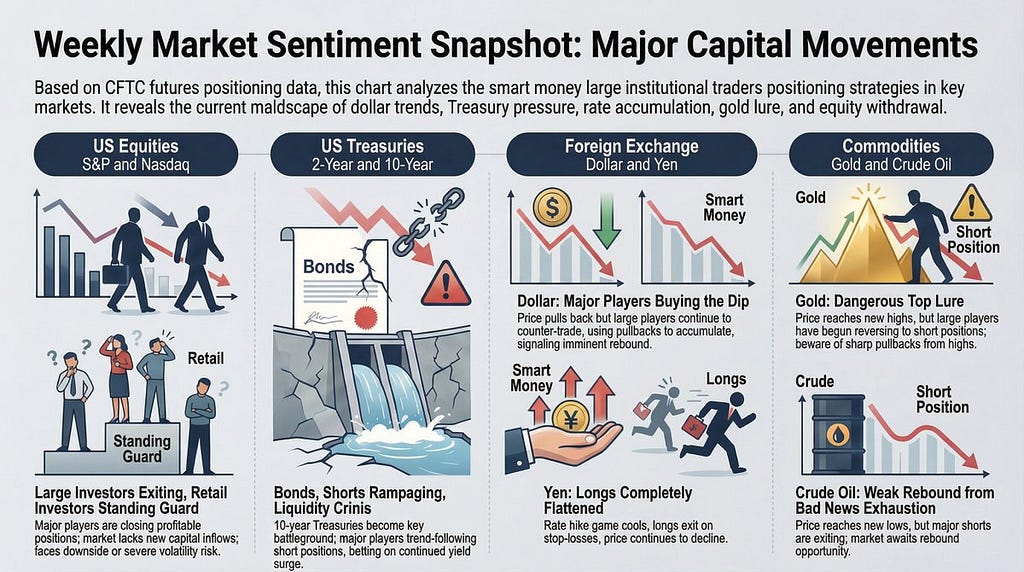

[Positioning & CFTC Data]

The USD is consolidating, Treasuries are in a liquidity crunch, Gold is a bull trap, and Equities are in retreat.

- U.S. Equities (S&P & Nasdaq): Large Players Exit, Retail “Holding the Bag.” Both indices show long-liquidation patterns. Smart money has locked in profits and is waiting, not yet shorting aggressively. Without new capital, retail cannot sustain these levels; expect a slow bleed or high-volatility churn next week.

- Treasuries (2Y & 10Y): Shorts Running Wild. Signals here are more ominous than in stocks. Large shorts are aggressively adding to 10Y positions — this. This isn’t just hedging; it’s a directional bet on higher yields.

- Forex (USD/JPY): The Main Battlefield. Smart money is buying the USD dip (Net positions rising despite price drops), while retail is “cutting losses.” Expect a USD rebound. Meanwhile, JPY loans are being liquidated as rate-hike bets fail.

- Commodities (Gold/Oil): The Lure of the Top. Gold shows classic “topping” characteristics: new price highs vs. shrinking net positions. Oil, conversely, shows “short covering” at new lows, suggesting $55–$60 is the floor.

[Moving Average Systems: Distribution After the Carnival]

Who is buying? Who is retreating? Treasuries are “bleeding,” the USD is “draining liquidity,” and the U.S. stocks are “tightrope walking.”

1/ S&P 500 (ES) & Nasdaq 100 (NQ): The “Hollowing Out” of Prosperity

Prices are being propped up, but institutional capital is withdrawing. The current rally is a low-volume game. Bullish momentum is exhausted; beware of a “flash-crash” style retracement. Chip distribution shows heavy overhead selling pressure. If moving average support fails, a sharp decline is imminent, with no solid “cover” until near 6800 (ES).

2/ U.S. Treasuries (US10Y/US02Y): The Return of Shorts

Stop dreaming of aggressive rate cuts! Yields stabilizing at 4.2% is just the beginning. Moving average calculation (backtesting values) is extremely low, meaning the trend will continue to push rates higher. Rates are “slow-acting poison” for high-valuation tech stocks.

3/ USD (DXY): The Loneliness of the Former Hegemon

DXY broke 98.50 support at high volume. Significant “trapped capital” is clustered above 100, meaning every rebound will face relentless selling from those looking to break even. Capital is fleeing to precious metals and non-USD currencies.

4/ Crude Oil (WTI): The Forgotten Corner

While precious metals skyrocketed, oil struggled at $60. The long-term channel confirms a bearish trend. $62 is a “minefield” of resistance, while $55 is the “iron floor.” Weak industrial demand has made oil the weakest link in the commodities complex.

5/ GC) & Silver (SI): This isn’t a Rally, it’s an “Exodus”

Gold is nearing $5,000, and Silver doubled in two weeks toward $100. Weekly moving average slopes are nearly 90 degrees vertical. People aren’t buying gold for “safety” anymore; they are buying it out of “distrust in fiat currency.” It is an irrational black hole with “only buyers and no sellers.”

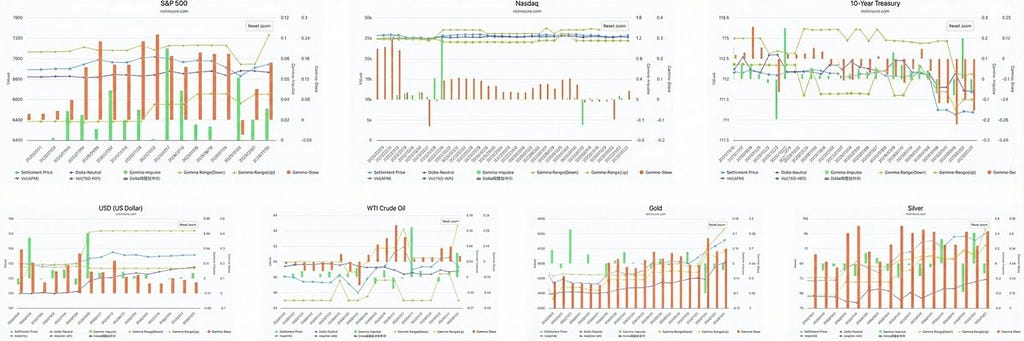

[Options Data]

Don’t catch the falling knife in bonds; don’t trust the calm in stocks; don’t chase the peak in gold; wait for a JPY bounce; oil depends on geopolitical “life support.”

- U.S. Equities: Surface calm masks institutional profit-taking and put-option hedging. The Nasdaq is fighting a “deadlock” at the equilibrium line. This wave is driven by retail FOMO, while institutions await the Fed and Big Tech earnings.

- U.S. Treasuries: Shorts are flooring the accelerator. Falling prices are met with passive hedging (Negative Gamma), amplifying volatility. Bottom-fishing Treasuries now is like trying to stop a truck on a highway.

- Gold & Silver: Speculative “boiling point.” Both have pierced the upper “Gamma-Range” ceiling. The silver rally is driven by sentiment and short-squeezes rather than value reversion. Once the bulls waver, the retracement will be violent.

- Japanese Yen (JPY): Currently extremely overbought, like a rubber band stretched to its limit. This deviation is unsustainable and suggests a violent mean-reversion toward normal pricing.

- WTI Crude: Purely “life support” from geopolitics. If tensions ease, fundamentals will pull it back to $55. Currently hitting the “Gamma-Range Up” ceiling at $60.37.

[Next Week Outlook]

This week, don’t look at inflation, look at nominees; don’t look at profits, look at AI spending; don’t look at the Fed, look at the White House.

- Mon-Fri: Fed Chair Nomination. Frontrunner Kevin Hassett’s “dove” reputation could spark rate-cut hopes, though it primarily shifts the long-end curve rather than immediate policy.

- Wed (1/28): Microsoft/Tesla Earnings + “Trump Account” Summit. Focus on AI monetization. Trump’s $1,000 “Baby Account” (helicopter money) is long-term bullish for consumption but may pressure long-end Treasury yields due to credit concerns.

- Thu (1/29): Fed Rate Decision + Apple/Meta Earnings. If Powell remains hawkish against near-term cuts, the USD will rebound strongly, and tech stocks face a “double whammy.”

- Fri (1/30): Dec PPI + Gov’t Shutdown Risk (1/31 Deadline). Polymarket predicts a 75% chance of a shutdown, which would trigger massive safe-haven demand.

Scenario 1: Nomination of New Leadership + Government Reaches Risk-Aversion Agreement

- Market Trend: Market returns to the “Growth Logic.” Hassett is nominated, and a government shutdown is averted.

- Asset Performance: US Dollar trends downward, US Treasuries turn bullish, and US Stocks (especially Tech stocks) embrace a primary upward wave.

- Action: Buy the dips on the Nasdaq and reduce US Dollar positions.

Scenario 2: Powell + Government Stuck in Shutdown Deadlock

- Market Trend: Market switches to “Defensive Mode.” Inflationary pressures lead Powell to deliver hawkish remarks, and political chaos intensifies.

- Asset Performance: US Dollar spikes on safe-haven demand, Treasury yield curve inversion deepens, and US Stocks enter an intermediate adjustment phase.

- Action: Cash is king. Buy volatility (VIX) and stay on the sidelines.